mycopula

Fitting Bivariate Copula (Step-by-step)

Now let’s start with the most basic thing which is how to fit the bivariate copula.

mycopula provides a very easy way to fit a bivariate copula. This will automatically output the most appropriate marginal distribution and copula functions from the listed functions.

Load Data

Let’s use the dataset provided by MATLAB: stockreturns, which consists of 10 observations from 10 stock assets.

load stockreturns

x1 = stocks(:,1);

x2 = stocks(:,2);

Marginal Distribution

The first step of the IFM method is to fit the distribution of each margin that will be used to fit the copula function. This is provided by the fitter function.

fitter(x): returns the fittest distribution of a vector column x.fitter(x,'sortby','value'): returns the fittest distribution of a vector column x, based on thesortbymeasurement.'value'can be'aic','adstat'(default), or'kstat'.fitter(x,'verbosity',value): returns the fittest distribution of a vector column x, with printing information about the fitting process.valuecan be 0 (prints no information), 1 (prints selected distribution information, default), or 2 (prints full information).fitter(x,'plotby',value): returns the fittest distribution of a vector column x, with outputting a comparison plot between the PDF of the selected distribution and its empirical histogram. 0 (default) no, or 1 yes.

The following is a selected distribution of data X1 and X2.

F1 = fitter(x1);

% ===== OUTPUT ======

Domain = Real

Sort by = Anderson-Darling Stastistics

fittest distribution = Logistic

Parameters: mu = -0.19364, sigma = 0.58158

Decision: fails to reject h0 (AD pval=0.9990)

F2 = fitter(x2);

% ===== OUTPUT ======

Domain = Real

Sort by = Anderson-Darling Stastistics

fittest distribution = Generalized Extreme Value

Parameters: k = -0.21362, sigma = 1.1975, mu = -0.66838

Decision: fails to reject h0 (AD pval=0.9949)

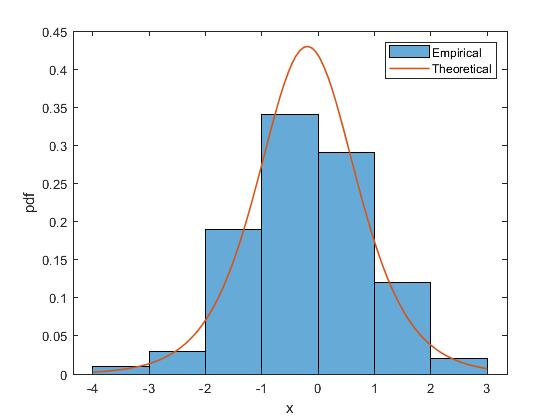

Then, here is an example of just outputting the PDF plot without printing the information.

fitter(x1,'verbosity',0,'plotpdf',1);

Probability Transformation

From the selected distribution function, the initial variable is transformed into a $\text{uniform}\sim(0,1)$ distribution.

u1 = cdf(F1,x1);

u2 = cdf(F2,x2);

Copula Fitting

The second step in the IFM method is to fit the copula function using transformed variables. This is provided by the copfitter function.

copfitter(U)returns the fittest copula of the matrix composed of the column vectors of the transformed variables. In the bivariate case,Ucan be written as[u1,u2].copfitter(U,'sortby','value')returns the fittest copula, based on thesortbymeasurement.'value'can be'aic'(default),'rmse', or'cvm'.copfitter(U,'verbosity',value)returns the fittest copula, with printing information about the fitting process.valuecan be 0 (prints no information), 1 (prints selected distribution information, default), 2 (prints top five copulas information), or 3 (prints full information).

This is an example of fitting a copula from a previously obtained variable.

C = copfitter([u1,u2],'verbosity',3);

% ===== OUTPUT ======

Case = Bivariate

Sort by = Akaike Information Criterion

Fittest copula = Gaussian

Parameter(s): param1 = 0.72231

Decision: fails to reject h0 (CvM pval=0.7361)

Summary =

copulaName param1 param2 CvM pValue RMSE AIC

________________ ___________ _______________ ________ ________ ________ _______

{'Gaussian' } 0.72231 {0×0 double } 0.020551 0.7361 0.014336 -71.733

{'Galambos' } 1.2566 {0×0 double } 0.022314 0.72827 0.014938 -70.995

{'Gumbel' } 1.9657 {0×0 double } 0.022681 0.72665 0.01506 -70.395

{'t' } 0.72216 {[ 2.9046e+06]} 0.020562 0.73605 0.01434 -69.733

{'BB1' } 0.17369 {[ 1.8277]} 0.021673 0.73111 0.014722 -69.294

{'BB1-180' } 0.80836 {[ 1.3924]} 0.023205 0.72435 0.015233 -69.126

{'BB6' } 1 {[ 1.9657]} 0.022681 0.72666 0.01506 -68.395

{'BB7-180' } 1.4889 {[ 1.3188]} 0.029178 0.6986 0.017082 -68.19

{'BB8' } 4.0639 {[ 0.8401]} 0.022983 0.72533 0.01516 -66.407

{'Frank' } 5.7461 {0×0 double } 0.023802 0.72174 0.015428 -64.383

{'Clayton-180' } 1.5251 {0×0 double } 0.048519 0.62134 0.022027 -62.997

{'BB8-180' } 2040.6 {[ 0.0028]} 0.023853 0.72151 0.015444 -62.369

{'Joe' } 2.3504 {0×0 double } 0.055282 0.59639 0.023512 -60.96

{'Galambos-180'} 1.1221 {0×0 double } 0.045016 0.63467 0.021217 -59.969

{'Gumbel-180' } 1.842 {0×0 double } 0.044492 0.63669 0.021093 -59.124

{'BB6-180' } 1 {[ 1.8420]} 0.044491 0.63669 0.021093 -57.124

{'Clayton' } 1.1633 {0×0 double } 0.1095 0.42937 0.033091 -46.108

{'BB7' } 1 {[ 1.1633]} 0.10949 0.42939 0.03309 -44.108

{'Joe-180' } 1.9989 {0×0 double } 0.12485 0.39125 0.035333 -41.478

{'Galambos-90' } -0.015625 {0×0 double } 0.67122 0.014272 0.081928 2

{'Galambos-270'} -0.0055666 {0×0 double } 0.67122 0.014272 0.081928 2

{'Joe-270' } -1 {0×0 double } 0.67122 0.014272 0.081928 2

{'Joe-90' } -1 {0×0 double } 0.67122 0.014272 0.081928 2

{'Clayton-270' } -1.4509e-06 {0×0 double } 0.67122 0.014272 0.081928 2.0002

{'Gumbel-270' } -1 {0×0 double } 0.67122 0.014272 0.081928 2.0002

{'Gumbel-90' } -1 {0×0 double } 0.67122 0.014272 0.081928 2.0003

{'BB8-270' } -1 {[ -1.0000]} 0.67122 0.014272 0.081928 4

{'BB8-90' } -1 {[ -0.9985]} 0.67122 0.014272 0.081928 4

{'BB6-90' } -1 {[ -1]} 0.67122 0.014272 0.081928 4

{'BB6-270' } -1 {[ -1]} 0.67122 0.014272 0.081928 4

{'BB7-270' } -1 {[-9.0917e-10]} 0.67122 0.014272 0.081928 4.0001

{'BB7-90' } -1 {[-1.5837e-08]} 0.67122 0.014272 0.081928 4.0001

{'BB1-90' } -2.2632e-09 {[ -1.0000]} 0.67122 0.014272 0.081928 4.0001

{'BB1-270' } -9.0917e-10 {[ -1.0000]} 0.67122 0.014272 0.081928 4.0001

For more convenience, we also provide copula fitting using only one line of code.

Download: this example is available on demo1.m. Visit Github

Visit my personal blog

@ 2021-2023 Mohamad Khoirun Najib